How to Buy a 2-Flat in Chicago and Have Your Tenant Pay Your Mortgage

How to Buy a 2-Flat in Chicago and Have Your Tenant Pay Your Mortgage

Buying a two-flat (duplex) property in Chicago and using the rent from your tenant to cover your mortgage is one of the most effective entry-level strategies for building wealth through real estate — especially for first-time buyers. This approach combines owner-occupied financing, rental income, and long-term equity growth in a single move.

Here’s a step-by-step roadmap to make it work.

What Is a Chicago 2-Flat?

A two-flat in Chicago is a single property with two separate residential units under one roof — often one unit on each floor. Many buyers live in one and rent out the other, which makes it an ideal house-hacking setup.

Why a Two-Flat Can Help You Live Mortgage-Free

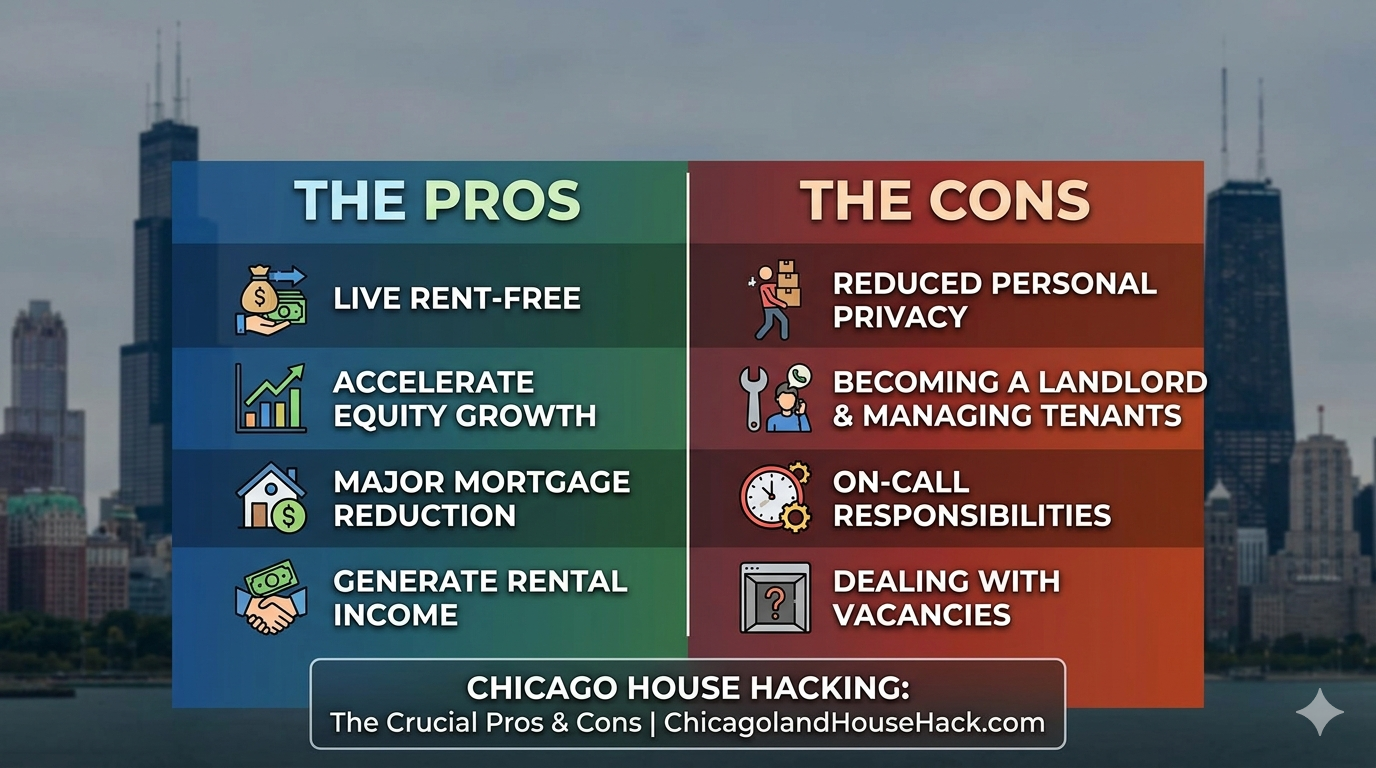

When you live in one unit and rent the other, the tenant’s rent can offset your monthly mortgage payment — and in some cases fully cover it. Many lenders will even include a portion of expected rental income in your loan qualification calculation, making the property easier to purchase in the first place.

Step 1 — Choose the Right Financing Path

FHA Loans (Low Down Payment)

- Buy 1–4 unit properties with just a 3.5% down payment

• Must live in one unit as your primary residence

• Lenders often count 75% of projected rent toward income for qualification purposes

• Great option for first-time buyers who want low upfront costs

Conventional Loans

- Minimum down payment is typically 5% or more

• Underwriters may still include rental income in qualification

• May require stronger credit or documentation than FHA does

VA Loans (For Eligible Borrowers)

- Zero down payment for 1–4 unit properties

• Rental income can boost qualifying power

• A strong option for veterans or eligible service members

Step 2 — Underwrite Rental Income Properly

Most lenders count about 75% of expected rent from the other unit(s) when qualifying you for a mortgage. This accounts for vacancies and maintenance costs. An appraiser estimates fair market rent based on comps and local data, helping lenders finalize underwriting.

Example:

If your tenant pays $2,000/month, lenders may count $1,500 of that as income toward your monthly qualifying totals — boosting your buying power and making approval easier.

Step 3 — Run the Numbers Before You Buy

To make sure your tenant truly pays your mortgage:

✔ Estimate monthly rent for the unit you’ll lease (use local comps)

✔ Subtract vacancy allowances (e.g., ~5-10%)

✔ Subtract operating costs (insurance, taxes, maintenance)

✔ Compare it against your mortgage payment

A well-underwritten two-flat should show you either break even or positive cash flow — meaning rental income can cover all or most of your mortgage.

Step 4 — Factor in Chicago Rules & Costs

Residential Landlord-Tenant Ordinance (RLTO)

If you plan to rent out a unit, you must comply with Chicago’s RLTO rules, which cover leases, security deposits, entry notices, repairs, and disclosures.

Permits & Code Compliance

Older two-flats often need inspections, proper permits, or renovations before closing — especially if there’s deferred maintenance or outdated systems. Factor these costs into your budget.

Step 5 — Prepare to Be a Landlord (or Delegate It)

Even if rent covers your mortgage, you still need a plan for:

- Tenant screening and leases

• Repairs and maintenance

• Rent collection systems

• Emergency fund for vacancies or big fixes

Some house hackers choose professional property management if they don’t want day-to-day tasks — especially in busy neighborhoods or with multiple units.

Why This Strategy Works in Chicago

Strong Rental Market

Chicago’s multi-unit housing stock and rental demand remain strong across many neighborhoods, which helps keep vacancy rates relatively low and rents competitive.

Entry With Equity Building

Unlike renting, every payment you make builds equity. When your tenant’s rent covers your mortgage, you’re effectively growing your net worth without adding to your monthly expenses.

Risks & What to Watch Out For

✔ Property condition unknowns — Always get a thorough inspection.

✔ Zoning or permit issues — Verify legal units before purchase.

✔ Vacancy periods — Budget reserves in case a tenant moves out.

✔ Market fluctuations — Rental markets can shift over time.

Being aware of these helps ensure your tenant’s rent really does cover your expenses and keeps your investment sound.

Final Thoughts: Turn Your Tenant Into a Mortgage Partner

Buying a Chicago two-flat with an intent to live in one unit and rent the other can help your tenant pay your mortgage, while you build equity and invest in your future. With the right financing, realistic underwriting, and attention to local city rules, this strategy turns housing costs into wealth-building opportunities.

👍 Bonus Tip: Before submitting an offer on your first two-flat, talk to a lender familiar with Chicago 2–4 unit underwriting — they can show you exactly how rental income affects your approval and monthly payments.

")

© 2026 Midwest Real Estate Data, LLC (MRED). The listing information is provided exclusively for consumers’ personal non-commercial use, and may not be used for any purpose other than to identify prospective properties consumers may be interested in purchasing. The data is deemed reliable but is not guaranteed by MTP or MRED. Listings courtesy of Midwest Real Estate Data, LLC as distributed by MLS GRID as of Friday, April 10th, 2026 at 05:20:28 AM. All data is obtained from various sources and has not been, and will not be, verified by broker or MRED. MRED supplied Open House information is subject to change without notice. All information should be independently reviewed and verified for accuracy. Properties displayed may be listed or sold by various participants in the MLS as established by the applicable MLS Governing Documents.

© 2026 Midwest Real Estate Data, LLC (MRED). The listing information is provided exclusively for consumers’ personal non-commercial use, and may not be used for any purpose other than to identify prospective properties consumers may be interested in purchasing. The data is deemed reliable but is not guaranteed by MTP or MRED. Listings courtesy of Midwest Real Estate Data, LLC as distributed by MLS GRID as of Friday, April 10th, 2026 at 05:20:28 AM. All data is obtained from various sources and has not been, and will not be, verified by broker or MRED. MRED supplied Open House information is subject to change without notice. All information should be independently reviewed and verified for accuracy. Properties displayed may be listed or sold by various participants in the MLS as established by the applicable MLS Governing Documents.