Chicago House Hacking: What to Look for When Buying a Multi-Unit Property (2026 Guide)

What is Chicago House Hacking?

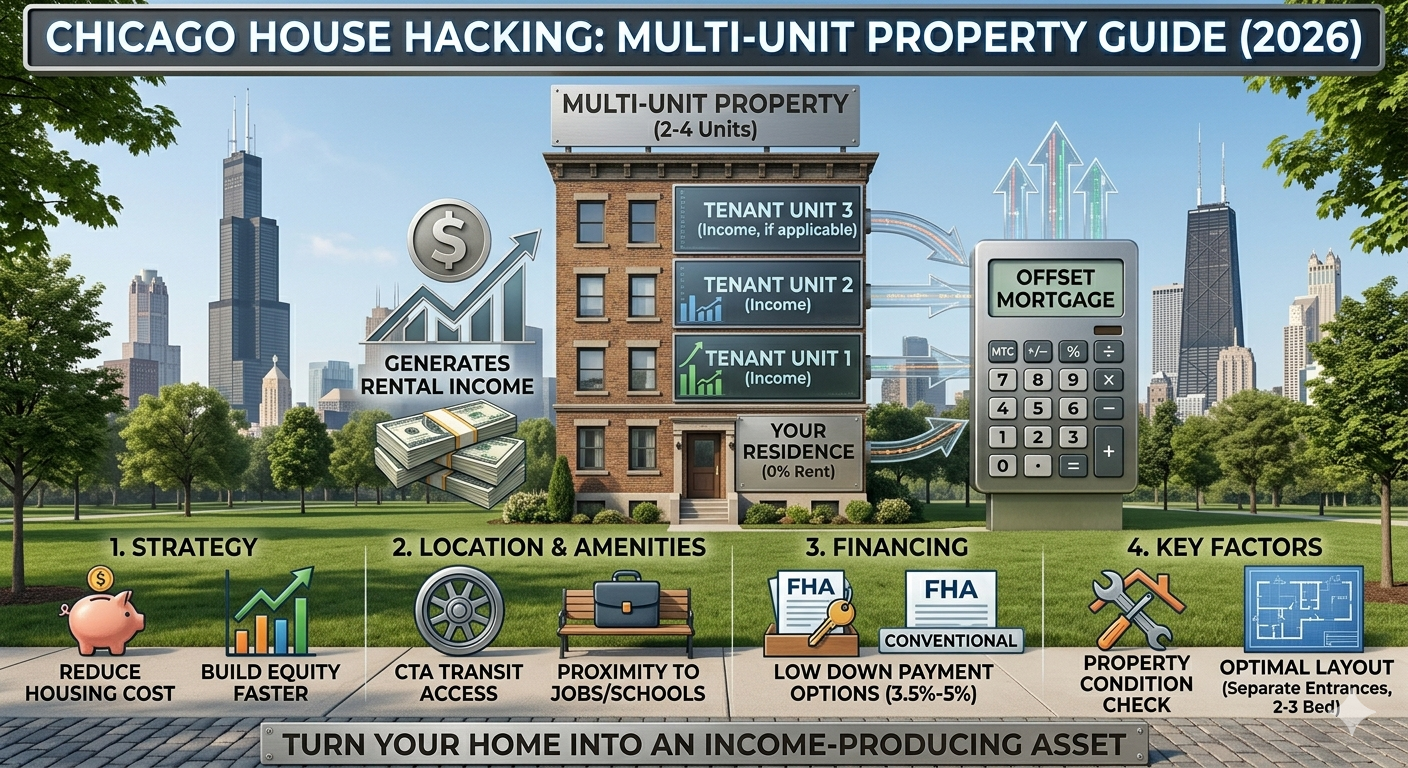

Chicago house hacking is one of the most powerful real estate strategies for new and experienced investors in Chicago.

It involves buying a 2-flat, 3-flat, or 4-unit property, living in one unit, and renting out the others to offset—or completely cover—your mortgage.

In a high-rent city like Chicago, house hacking allows buyers to:

- Reduce or eliminate housing costs

- Build equity faster

- Generate rental income from day one

- Qualify for owner-occupied financing (low down payment options)

Many investors use FHA or conventional owner-occupied loans with as little as 3.5%–5% down.

Many investors use FHA or conventional owner-occupied loans with as little as 3.5%–5% down.

Why Chicago is One of the Best Cities for House Hacking

Why Chicago is One of the Best Cities for House Hacking

Chicago remains one of the strongest markets in the U.S. for multifamily owner-occupants because:

- High rental demand across most neighborhoods

- Strong population density

- Affordable entry price vs coastal cities

- Large supply of 2–4 unit buildings

- Stable long-term appreciation trends

In many Chicago neighborhoods, a 2–4 unit property can generate $3,000–$6,000+ monthly gross rent, depending on condition and location.

1. Location (Most Important for House Hacking Success)

1. Location (Most Important for House Hacking Success)

For Chicago house hacking, location determines both your comfort and your rental income.

Look for:

- Safe, tenant-friendly neighborhoods

- Access to CTA trains and buses

- Proximity to jobs, schools, and hospitals

- Low vacancy rental zones

- Strong rent-to-price ratio

Investor insight: Areas near transit corridors often outperform by 10%–20% higher rent demand stability.

2. Property Condition (Avoid Hidden Cost Traps)

2. Property Condition (Avoid Hidden Cost Traps)

Older Chicago multi-units often look like great deals—but repairs can destroy cash flow.

Major cost risks:

- Roof replacement: $8,000–$25,000

- Plumbing system updates: $5,000–$20,000

- Electrical rewiring: $3,000–$15,000

- Foundation repairs: $10,000–$40,000

Must-check items:

- Roof age and leaks

- Basement water issues

- Electrical panel safety

- Furnace and HVAC condition

- Lead or outdated plumbing

Around 1 in 4 older multifamily homes in Chicago require major rehab within 3 years of purchase.

3. Layout Matters for House Hacking Efficiency

3. Layout Matters for House Hacking Efficiency

Not all 2–4 unit buildings perform the same.

Best layouts for house hacking:

- Separate entrances per unit

- 2–3 bedroom layouts

- Private utilities (gas/electric/water if possible)

- Functional kitchens and living space

- Good natural light

Units with tenant-paid utilities can reduce owner expenses by 15%–30%, increasing net cash flow significantly.

4. Rental Income vs Mortgage (The House Hacking Formula)

4. Rental Income vs Mortgage (The House Hacking Formula)

The core of Chicago house hacking is offsetting your mortgage.

Example scenario:

- Purchase price: $450,000

- Down payment: 5% ($22,500)

- Total rent (3 units): $3,600/month

- Mortgage + taxes + insurance: $3,200/month

Result: You live almost free or with minimal housing cost.

5. Cash Flow and Operating Expenses

5. Cash Flow and Operating Expenses

Even if you live in the property, it must still be a good investment.

Typical monthly expenses:

- Property taxes: 10%–25% of income

- Insurance: $150–$400/month

- Maintenance reserve: 5%–10%

- Vacancy allowance: 5%–8%

- Repairs and capital expenses

Strong house hacking deals still maintain positive or near-zero living cost after expenses.

6. Market Rent Analysis (Hidden Profit Lever)

6. Market Rent Analysis (Hidden Profit Lever)

One of the biggest mistakes buyers make is ignoring rent gaps.

Example:

- Current rent: $1,200/unit

- Market rent: $1,600/unit

- Upside: +$400/unit

For a 3-unit building:

- $14,400/year in unrealized income

This is where investors build equity without renovation.

7. Financing Advantages of House Hacking

7. Financing Advantages of House Hacking

Chicago house hacking is powerful because of owner-occupied loan options:

- FHA loans (3.5% down)

- Conventional 5% down owner-occupied loans

- Lower interest rates vs investment loans

- Easier qualification requirements

You must live in the property for typically 12 months to keep owner-occupied benefits.

Final Thoughts

Final Thoughts

Chicago house hacking is one of the fastest ways to build wealth in real estate.

The key to success is not just buying any 2–4 unit property—but analyzing:

- Location strength

- True repair costs

- Rental income potential

- Financing structure

- Long-term cash flow stability

When done correctly, house hacking allows you to turn your primary residence into an income-producing asset.

FAQ (Chicago House Hacking)

FAQ (Chicago House Hacking)

What is Chicago house hacking?

Chicago house hacking is when you buy a multi-unit property, live in one unit, and rent out the others to offset your mortgage.

How much do I need to start house hacking in Chicago?

You can start with as little as 3.5% down (FHA loan) if you qualify, plus closing costs.

Is Chicago good for house hacking?

Yes. Chicago is one of the best U.S. cities due to affordable multifamily properties and strong rental demand.

What type of property is best for house hacking?

2–4 unit buildings (2-flats, 3-flats, 4-flats) are the most common and effective for house hacking.

Can house hacking cover my entire mortgage?

In many Chicago neighborhoods, yes—if rental income is strong and expenses are controlled.

© 2026 Midwest Real Estate Data, LLC (MRED). The listing information is provided exclusively for consumers’ personal non-commercial use, and may not be used for any purpose other than to identify prospective properties consumers may be interested in purchasing. The data is deemed reliable but is not guaranteed by MTP or MRED. Listings courtesy of Midwest Real Estate Data, LLC as distributed by MLS GRID as of Friday, April 10th, 2026 at 05:20:28 AM. All data is obtained from various sources and has not been, and will not be, verified by broker or MRED. MRED supplied Open House information is subject to change without notice. All information should be independently reviewed and verified for accuracy. Properties displayed may be listed or sold by various participants in the MLS as established by the applicable MLS Governing Documents.

© 2026 Midwest Real Estate Data, LLC (MRED). The listing information is provided exclusively for consumers’ personal non-commercial use, and may not be used for any purpose other than to identify prospective properties consumers may be interested in purchasing. The data is deemed reliable but is not guaranteed by MTP or MRED. Listings courtesy of Midwest Real Estate Data, LLC as distributed by MLS GRID as of Friday, April 10th, 2026 at 05:20:28 AM. All data is obtained from various sources and has not been, and will not be, verified by broker or MRED. MRED supplied Open House information is subject to change without notice. All information should be independently reviewed and verified for accuracy. Properties displayed may be listed or sold by various participants in the MLS as established by the applicable MLS Governing Documents.